Conventional formwork proppring system is different from the system formwork.

The above photo is the conventional propping method. The typical erection with a contraint of a limitation of height of propping from the supporting base to the top.

A horizontal 2"x3" timber is supporting the span in the required interval of spacing of 2 feet or more, depend on the beam size and height.

Two diagional branch supports are firmly nailed to connect the horizontal 2"x3" support and vertical 2"x3" strut. The centre 1"x2" is forming the T- propping.

The magic portion is the wedges slot in between the both sides of the beam to prevent the beam bulging and secure the bottom size of beam.

Things need to be taken note here are the width of the beam must carefully take into the consideration as the prefabrication of the propping size must be firmly fix to secure the bottom of beam.

The second thing is the height of the beam must be approximately 8-12 feet, as if higher beam shall replace the propping either scaffolding or closer spacing of prop.

This kind of conventional propping is normally used in the normal housing project as the floor to floor height is consistent and about 8-12 feets height only.

Besides the cost of timber is cheaper than other system formwork, the portable size of light propping is another encourage point.

Wondering can this kind of timber propping material to replace by those steel support as the durability and recycling times are soon to be one of the important factor to be consider.

Timber formwork will be obsolete while cost of the steel form comparatively go lower than timber.

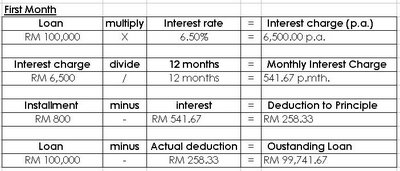

Then, the subsequent months will be follow with the above formula. When the outstanding loan become ZERO, there is the settlement of loan and total months of repayment is the whole loan tenure.

Then, the subsequent months will be follow with the above formula. When the outstanding loan become ZERO, there is the settlement of loan and total months of repayment is the whole loan tenure.

An example of pile cap is shown at the above.

An example of pile cap is shown at the above.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}